Providing Strategic & Innovative

Solutions to Sensitive Tax Problems

Solutions to Sensitive Tax Problems

The Internal Revenue Service (IRS) must abide by the statutes of limitations established by the Internal Revenue Code to analyze, review, and resolve tax-related issues. When the statute of limitations expires, the IRS may no longer take action in particular ways, including assessing additional tax or taking a collection action. The statute of limitations is different depending on whether the matter involves an assessment, refund, collection, or criminal tax prosecution. The California Franchise Tax Board (FTB) has different deadlines within which to propose additional taxes or assessments. If you are concerned about a statute of limitations issue, the Los Angeles tax lawyers at the Ben-Cohen Law Firm can provide sophisticated and detailed legal advice.

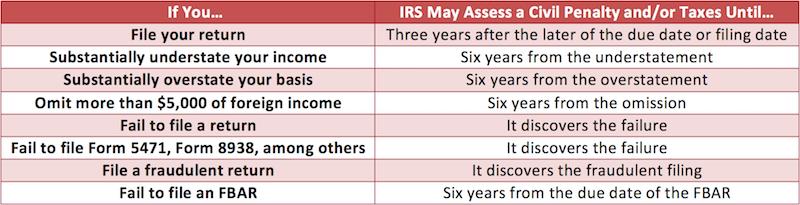

The IRS statute of limitations related to assessing income taxes differs depending on whether you filed a tax return, as well as whether that return was accurate. In general, if you did file a return, the IRS has three years from the due date of the return or the date on which it was filed, whichever comes later, to determine whether you owe additional taxes. However, the FTB generally has four years from the original April 15 due date of the return to assess taxes. In cases where a taxpayer has not filed the return on or before the due date, the FTB has four years from the date that the return was filed to assess tax.

Federal tax assessments require an IRS officer to sign a certificate of assessment, stating what is still owed by the taxpayer. If you file a return that is not accurate, the IRS has three years to require you to pay the taxes that it believes you owe. One exception is when the IRS finds a substantial omission of more than 25% of gross income on the return, in which case the statute of limitations is six years after the return was filed. In addition, there is no time limit for the IRS or FTB to assess income tax if a taxpayer did not file a tax return or filed a false or fraudulent return.

Once the IRS assesses income taxes, it has 10 years within which to collect the assessed taxes. The IRS has numerous methods of tax debt collection, including wage garnishment and levies. Interest and penalties may be added onto the original amount owed. However, certain events stop the 10-year statute of limitations from running, including filing for an appeal, filing for bankruptcy, litigation against the IRS, an offer in compromise, and a collection due process hearing. If you have lived abroad for six consecutive months or more, that period may also prolong the 10-year statute of limitations for federal taxes. Under California Revenue and Taxation Code Section 19255, the statute of limitations to collect unpaid state tax debts is 20 years from the assessment date, but there are situations that may extend the period or allow debts to remain due and payable.

The stakes are particularly high in criminal tax prosecution cases. This is especially true when the IRS is able to prove that someone filed a fraudulent tax return or willfully tried to evade paying taxes or filing a return. Internal Revenue Code Section 6531(2) states that the statute of limitations for criminal tax prosecution is six years, commencing once the return is filed or from the time that a taxpayer willfully failed to file a return.

There are heightened penalties involved when an individual’s actions related to taxes are willful or intentional, and in some cases a taxpayer may face criminal charges, such as for tax fraud or tax evasion. An experienced attorney can help a taxpayer determine whether they should come forward voluntarily to pay back taxes and determine the risk of criminal penalties.

Many taxpayers face issues related to the statute of limitations for assessment, refund, collection, or criminal tax prosecution. Our Los Angeles attorneys can provide knowledgeable counsel and representation, whether you are dealing with civil or criminal tax matters. Mr. Ben-Cohen is an attorney, a CPA, and a Board Certified Taxation Law Specialist who can provide you sophisticated legal advice regarding your statute of limitations issue. Contact us at (310) 272-7600 or complete our online form to set up an appointment with a collection defense attorney or seek representation in another matter related to your tax obligations. We assist taxpayers in Santa Monica, Malibu, Beverly Hills, Burbank, Pasadena, Sherman Oaks, Venice, and West Hollywood, as well as other areas of Los Angeles County.